Executive Summary: Burgundy 2018 Vintage

- CW Burgundy outperformed Liv-ex’s Burgundy 150 over the last 5 years benefiting from our more diversified approach to the region, in particular with an allocation to selected up-and-coming producers.

- Burgundy is considered as more complex than any other wine regions: niche market knowledge and a selective approach do enhance returns and reward the patient investor.

- Exports of Burgundy rose to €1 billion for the first time in history last year.

- Burgundy is the ultimate representation of supply and demand imbalance in Fine Wine.

- Domaine Armand Rousseau achieved 1st place in the recently published Liv-ex the Power 100 list and a record 10 out of the 18 new entrants, were producers from Burgundy.

- Whilst return sustainability concerns have affected the top names, we believe there is scope for continued upside for Burgundy prices in both medium and long term.

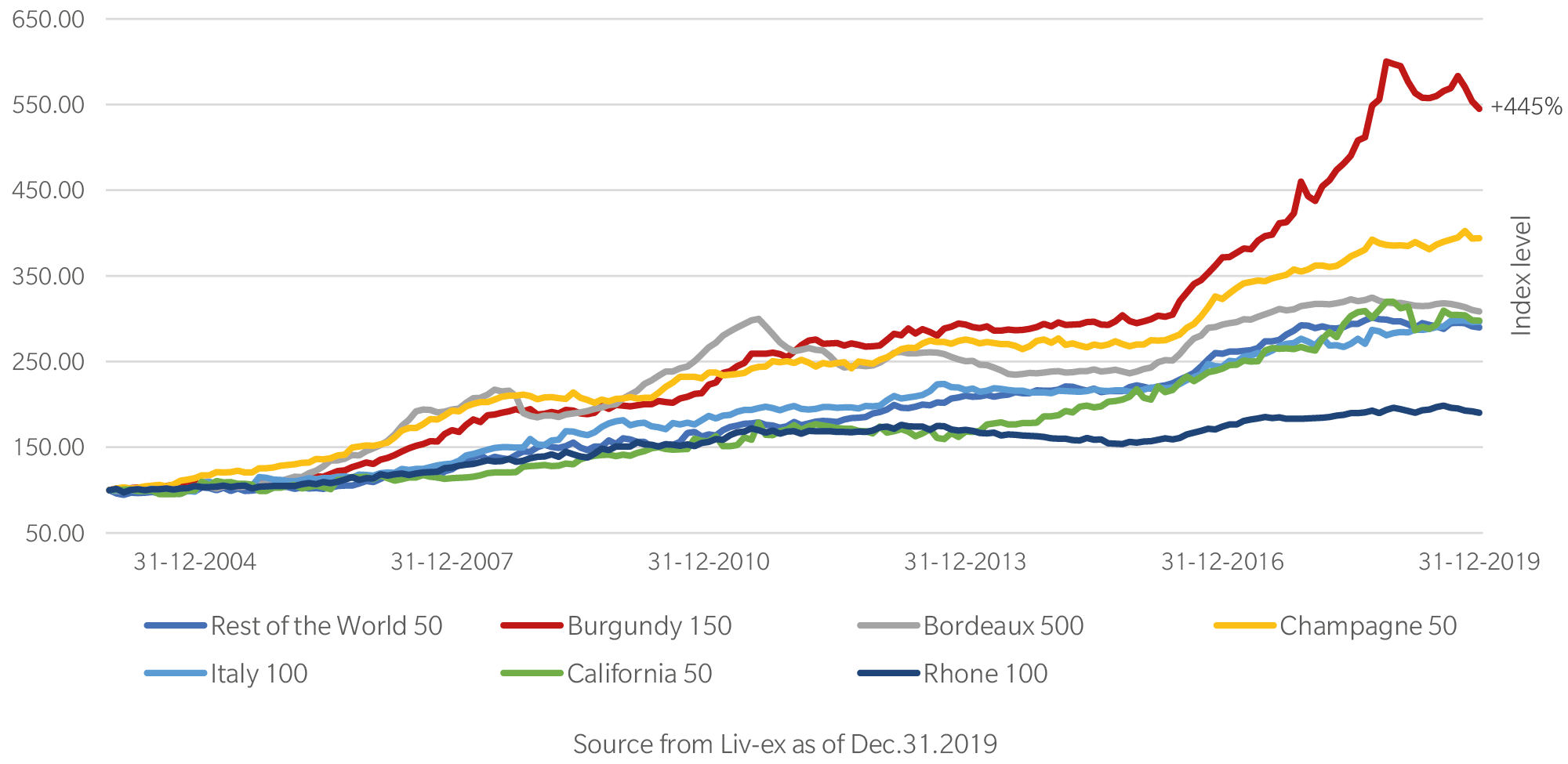

Exhibit 1 Burgundy outshone other sub-regions over the last 15 years

Why invest in Burgundy EP 2018 with Cult Wines?

CW Burgundy index contains 129 unique producers, representing more than 500 Burgundies irrespective of vintages. It is a well-diversified portfolio across vineyards and vintages, offering exposure to a wide range of opportunities at varying price points and with different investment profiles.

As illustrated in the table above, Cult Wines’ Burgundy index has outperformed Liv-ex’s Burgundy 150 index over the last five years: 14.5% vs 13.4% per annum. Our selective approach in conjunction with a diversified strategy has always been a critical factor in providing consistent, strong returns for our investors.

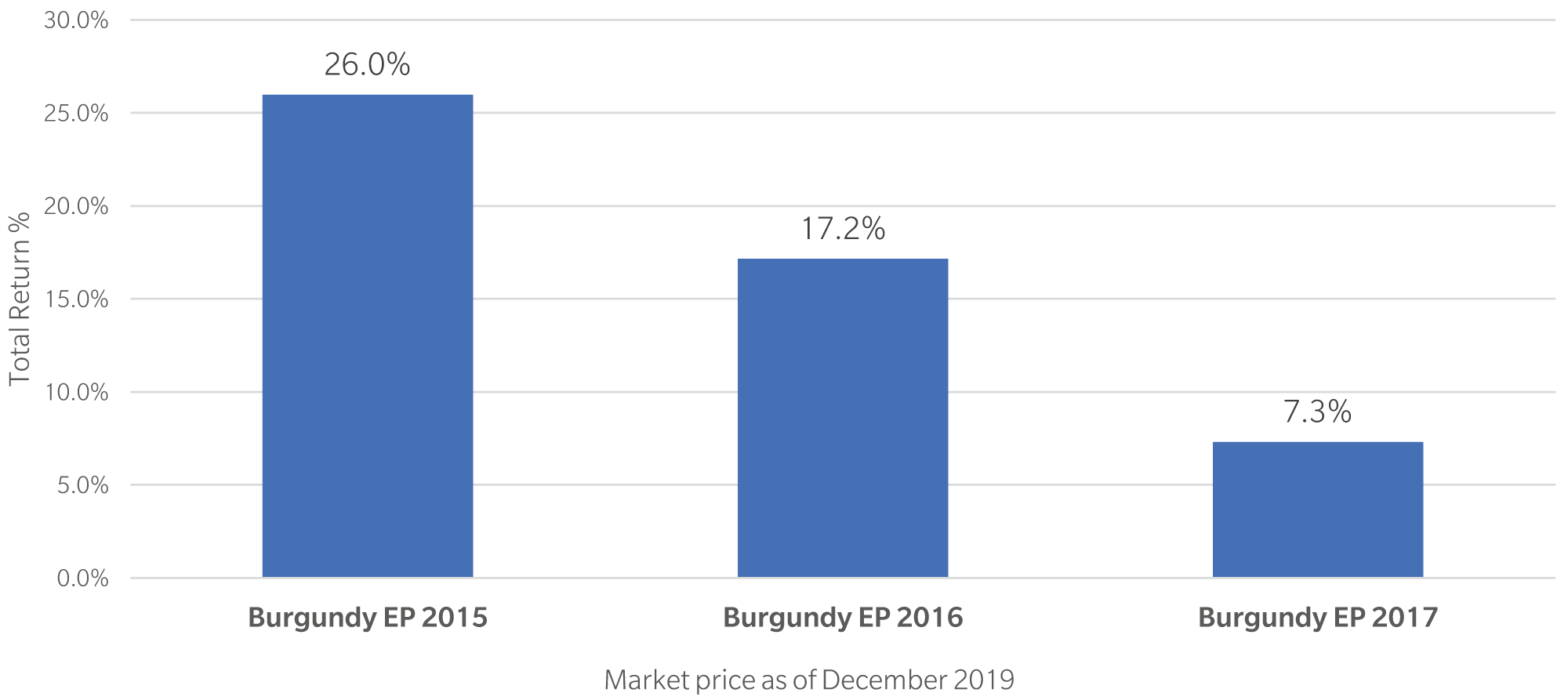

Exhibit 2 Cult Wines Burgundy EP Performance

NB A wine will be released two years after its vintage, e.g. Burgundy EP 2015 occurred in 2017

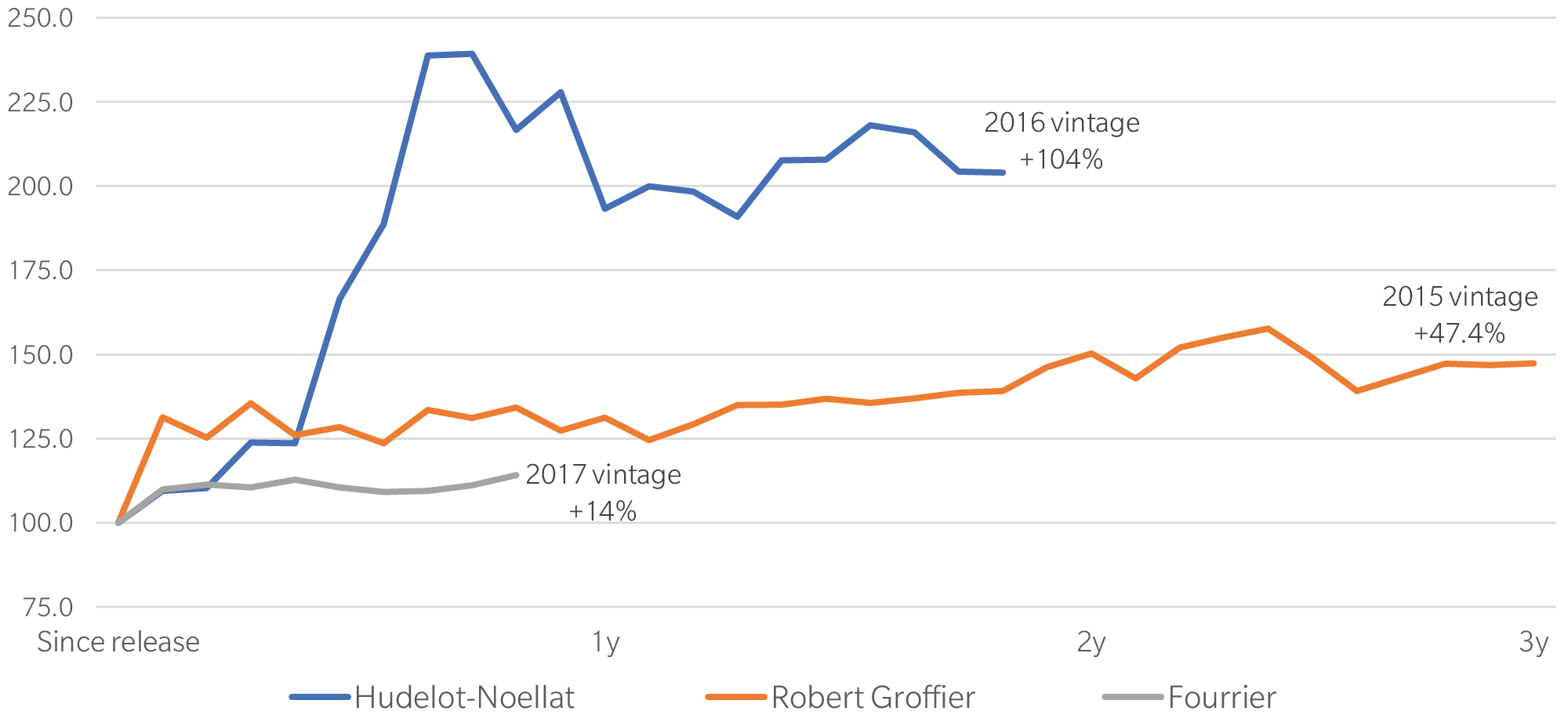

For Burgundy En Primeur (EP), wines from selected producers are added into CW portfolios if they meet strict criteria: solid fundamentals with potential to grow steadily yet faster than the broader market. We believe that buying the right producers in EP is crucial to performance as wines tend to be unavailable at a later stage or increase in price rapidly. For example, Domaine Hudelot Noellat has demonstrated strong performance, delivering a total return of 104% since our 2015 EP purchase. Fourrier, which we selected in 2017 EP, has risen by 14% in just over a year.

Exhibit 3 Cult Wines Selected Burgundy Producers EP Performance 15/16/17

Investment View on Burgundy

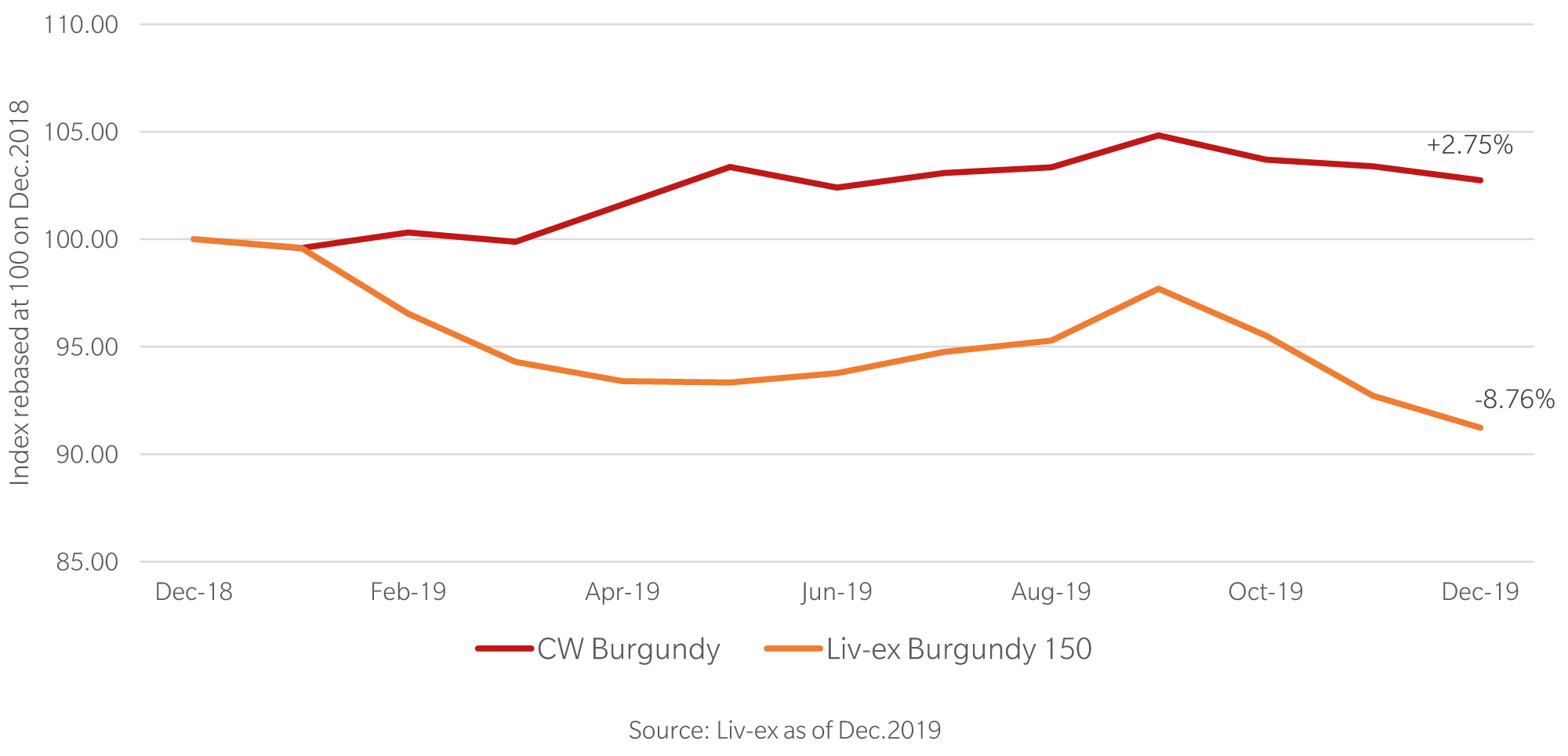

We expect 2020 to be a defining year for Burgundy. The sustainability of the rising market has come into question over the last few months. Many investors have expressed concern about Burgundy being vulnerable to a general slowdown, with the Liv-ex’s Burgundy 150 dropping the most in 2019 compared to the other sub-indices. With DRC accounting for 60% of the index constituents, it is believed that top Burgundies will be highly sensitive to any change on investor’s sentiment behind the trend. As some iconic Burgundies have come under pressure after a quick rise in value, a selective approach is strongly called for. Meanwhile, opportunities linked to the search for untapped value in the region should also start to emerge. The outperformance of CW Burgundy index over Liv-ex’s Burgundy 150 suggests that ongoing demand for Burgundy and high prices for iconic producers will lead to broadening interest for second tier and up-and-coming producers.

Exhibit 4 Cult Wines Burgundy out-performed Liv-ex Burgundy 150 in 2019

Burgundy may appear to be more complex and fragmented than other regions, but with niche market knowledge and a selective approach, investors will be greatly rewarded over time. As highlighted in our Investment Outlook 2020, our overweight stance to Burgundy is supported by growing demand and fundamental scarcity. More importantly, strict allocation policy is a positive for investors who can commit capital for the En Primeur release period when the wine is still in the barrel and wines are at their most affordable.

Liv-ex Power 100 list - What changed from 2018 to 2019?

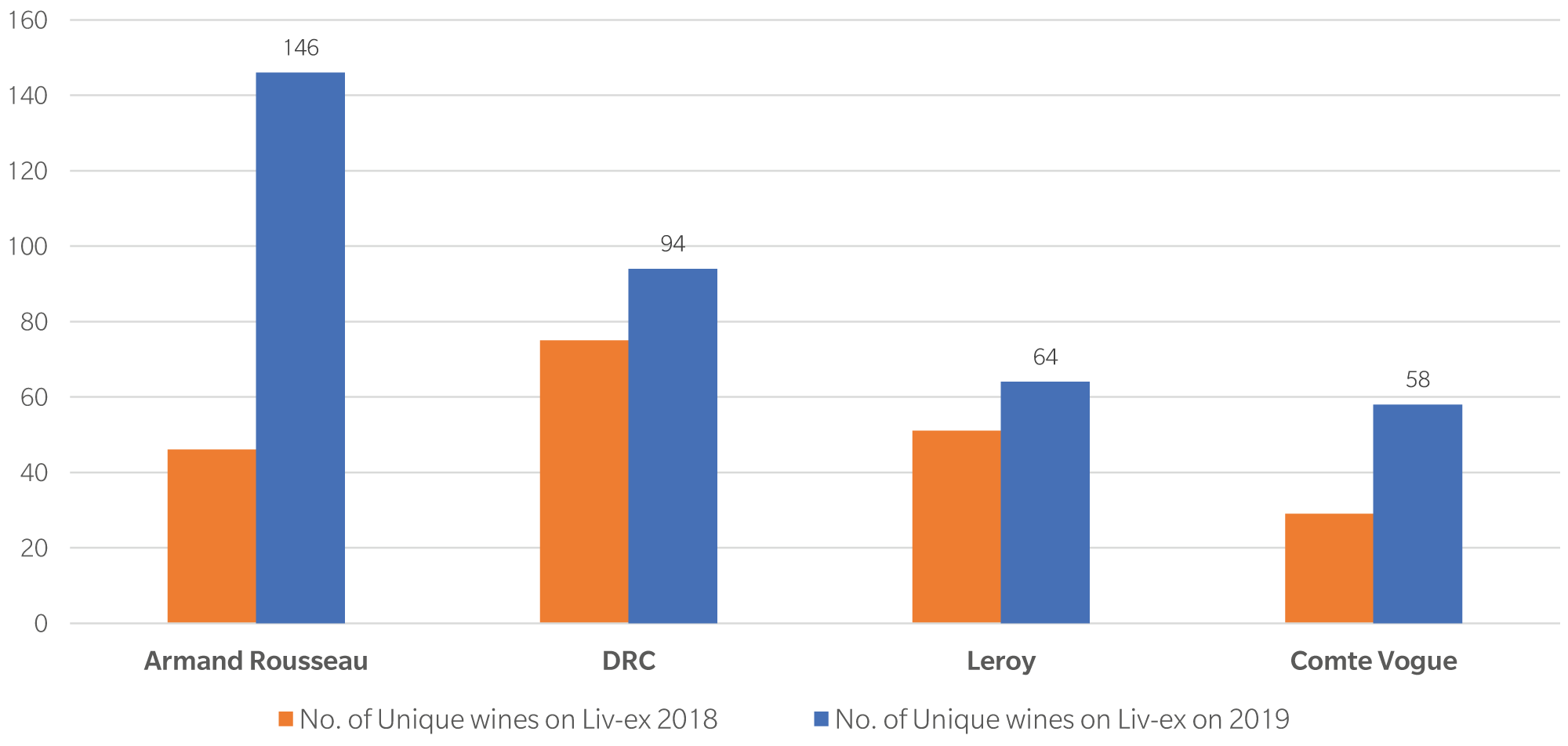

In January this year, Liv-ex has published the 14th edition of the Power 100 – the annual list of the most powerful brands in the fine wine market in 2019. Armand Rousseau topped this list for the first time, but is no newcomer: it was ranked No. 7 in 2018 and No. 8 in 2017. Particularly with Burgundy, that consistency is not typical of the Liv-ex Power 100 list. Recent years’ results have suggested that the interests of market participants have spread from DRC, which traditionally dominate the Burgundy trading market, to other well-respected producers. This year, Burgundy has made its presence truly felt in the wine investment market, with 13 new entrants (out of 18 in total) from the region being added to this list, indicating a widening of interest beyond the iconic producers.

Apart from price performance, trading activity on the secondary market is also considered an important factor when determining producers’ growth potential. Among the top 3 wines on this year’s Power 100 list, we noticed that the biggest increase, compared to 2018, can be seen in the number of unique wines traded on Liv-ex from Armand Rousseau, up from 46 to 146 – an impressive 217% (Exhibit 5). In 2010, 68% of the wines that traded on Liv-ex were from Bordeaux, they now represent only 37% of trade and wines from Burgundy and other important regions are catching up 1. In particular, the Burgundy offering has risen significantly, with its number of individual wines trading on Liv-ex standing at 1580 by the end of 2018, jumping from 248 in 2010.

Exhibit 5 Armand Rousseau has seen the biggest rise on numbers of wines trading on Liv-ex

Exports of Burgundy exceeded 1 billion EUR for the first time in 2019, according to the Drinks Business. Hong Kong and Japan have seen good growth (measured by value), indicating growing demand for top Premier and Grand-Cru wines from those markets 2.

CW retained its overweight stance on Burgundy for 2020, with a special focus on second tier and up-and-coming producers. Last year, prices for top-Burgundies were growing at a slower pace than a year ago. At the same time, second tier producers and up-and-coming producers have shown potential.

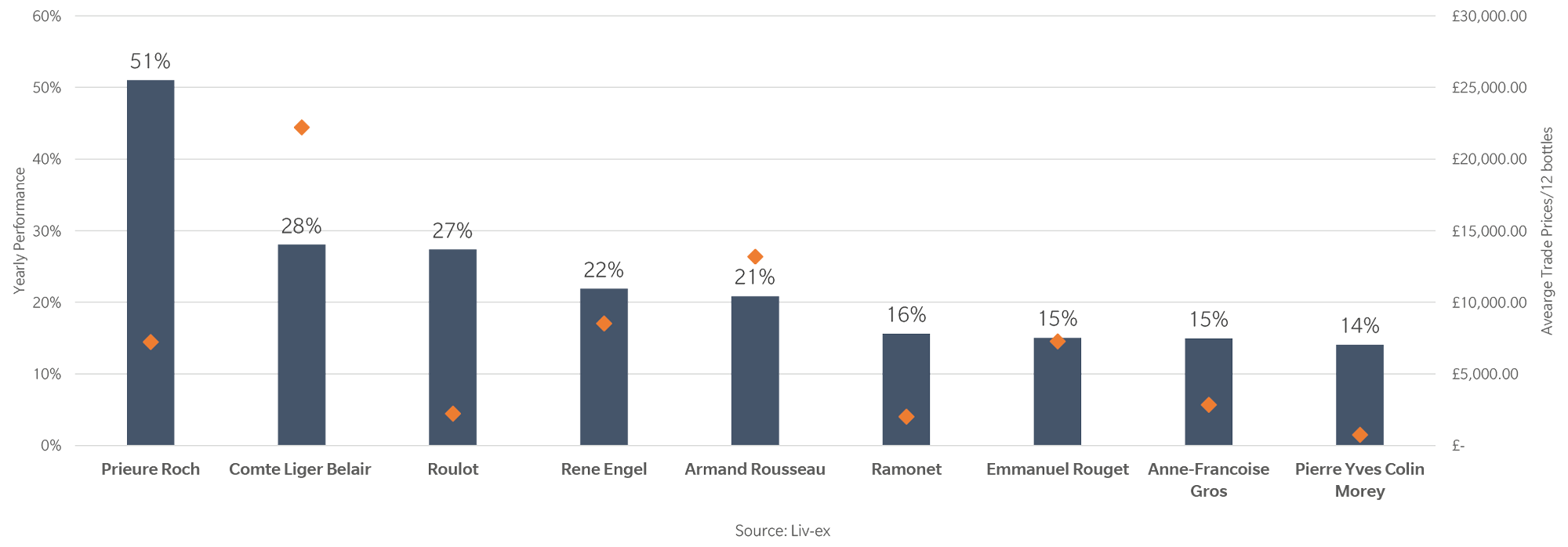

To demonstrate this shift in landscape further, we have compared the relative value, as measured by yearly increase in value, of Liv-ex’s top-performing Burgundies in 2019. As shown in Exhibit 3, except for Armand Rousseau and Domaine du Comte Liger-Belair, which boast the highest priced wines on the list, we have witnessed that most of the excess returns of the region came from Burgundies whose average trade price on Liv-ex are under £10,000 per case of 12 bottles (Exhibit 6). All told, in a broadening wine market, looking beyond iconic producers and being selective on second-tier producers in Burgundy is the right strategy to adopt.

Exhibit 6 Best-performing Burgundies on the Power 100 list

1https://www.liv-ex.com/2019/07/diverse-market-fine-wine/

2https://www.thedrinksbusiness.com/2019/12/burgundy-exports-top-e1bn-for-first-time/

Cult Wines Investment Team discuss the current price disparity created by top tier Burgundy producers

CW Approach to Burgundy EP

In the past 10 years, Burgundy prices have taken off to stratospheric levels. This would only be possible if the wines of the region consistently performed to an ever-raising standard of expectation. The combination of quality, history, terroir and low production when put together make for a wine that is spectacular to drink while also being a lucrative investment.

However, to generate returns in a segmented market like Burgundy, a selective and producer-specific strategy is strongly called for. Diversification and return potential have always been an important rationale behind our investment strategy and we are always expanding our target universe to the up-and-coming producers of the market. By moving beyond Tier 1 producers, investors in Burgundy can gain meaningful exposure to the producers which will profit from continued demand for the region at lower entry prices.

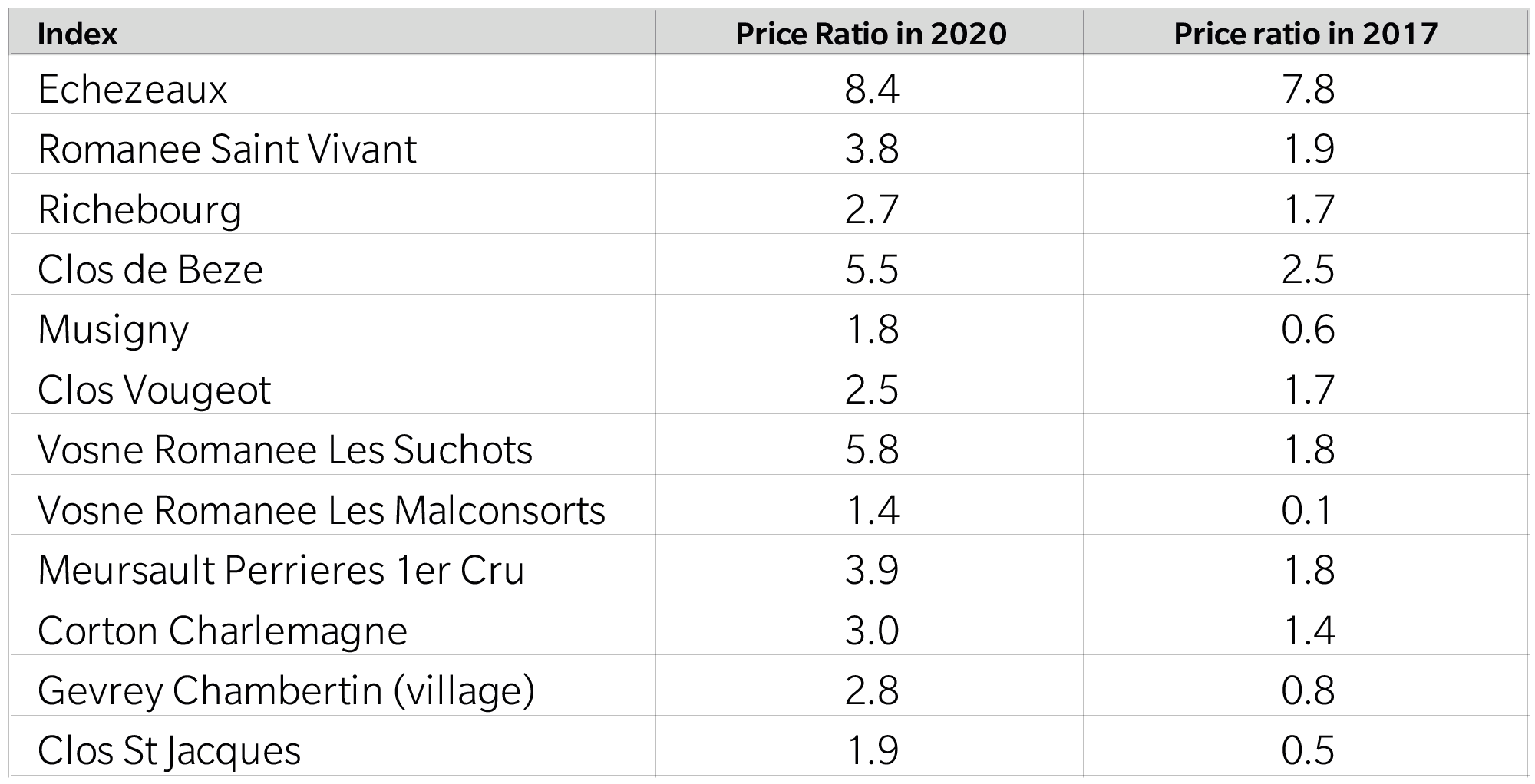

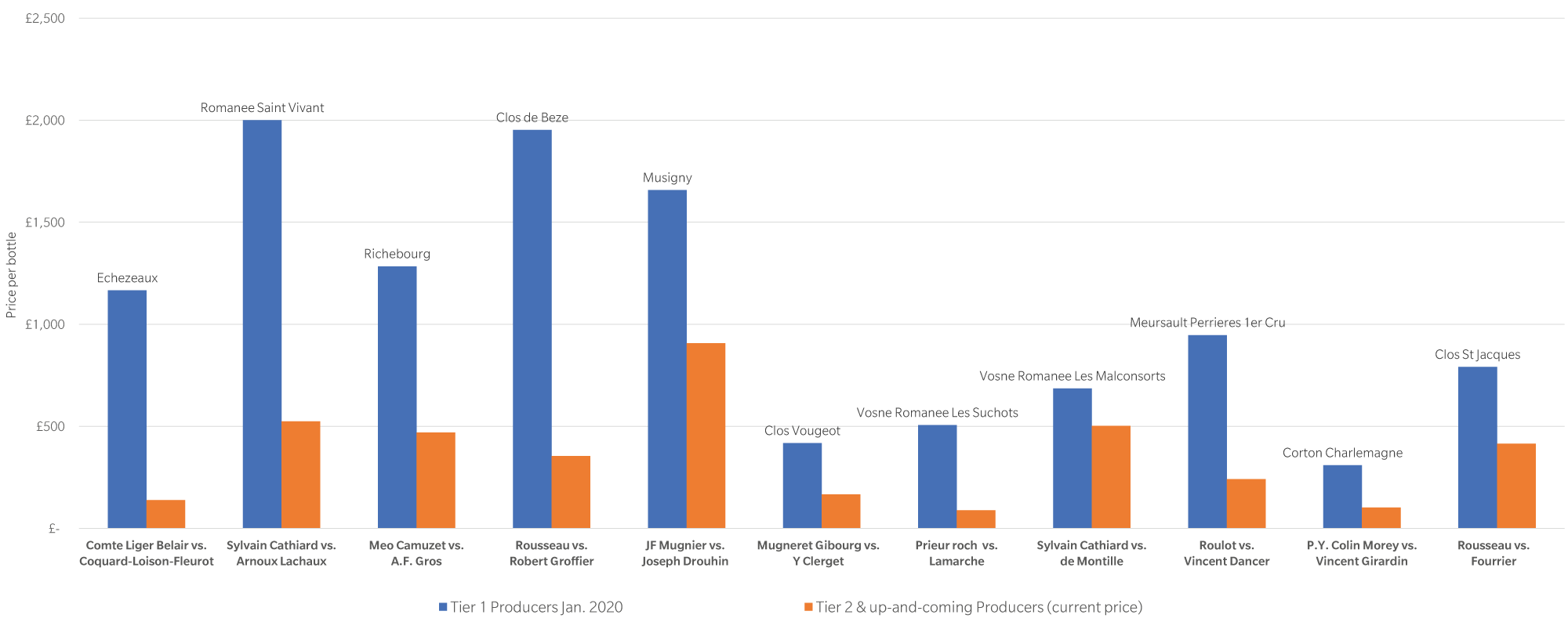

The table below shows the price difference between Tier 1 (iconic) and Tier 2 (rising star) producers from the same vineyard. Due to the dramatic price increase of Tier 1 wines over the past 3 years, the price disparity (price ratio) has changed substantially. Each pair included for comparison is based on the producer’s reputation, price differential and comparable quality (critic scores). Using both this and the graph below, one can make a solid conclusion that prices for iconic Burgundies have risen far faster than their peers over the last three years. Due to the now very large price differential, we expect these high-quality Tier 2 producers to rapidly close this gap.

Exhibit 7 Wide price gap between Tier 1 and Tier 2 producers could be an opportunity - Price comparison

In particular, Romanee Saint Vivant and Clos De Beze show the biggest price difference on a Grand-Cru level, with the price ratio more than doubling over the past three years between the top producers (Rousseau, Cathiard) and their counterparts (Groffier and Arnoux Lachaux) a great opportunity for those who invest in Burgundy presents itself as we expect this price gap to close, as both consumers and collectors look for greater value within the best vineyard sites. Premier Crus such as Vosne Romanee les Suchots and Meursault Perrieres are also demonstrating a great degree of potential. The market inefficiency implied in this price ratio should normalize: investors will benefit from this disparity as prices for Tier 2 producers catch up with their peers.

This highly selective strategy encapsulates not only a quantitative but also our qualitative approach to allocation – isolating producers where the quality is equivalent to their far higher priced counterparts, as well as trends of increased global consumption and popularity. Essential with Burgundy’s minute production.

It stands to reason that if Cathiard RSV costs £2,000 per bottle now, and Arnoux Lachaux’s RSV, a wine with the equivalent score and rapidly growing demand in Asia (for example) costs £500, that gap will begin to rapidly diminish, rewarding the investor.

Concluding Thoughts

En Primeur is both the most cost efficient and only time you will be able to access the wine which we have determined to have this scope. With production in hundreds, rather than thousands of cases, and rapid price rises after the campaign, it is imperative that any investor wishing to benefit from these returns commits capital now.